Introduction to Modern Portfolio Theory

The modern portfolio theory helps in maximising the return of a portfolio by selecting the right investments. The Nobel Prize-winning economist, Harry Markowitz, is best known for his contribution to “Modern Portfolio theory”. The key concept of the MPT is diversification. Generally, higher risk fetches higher reward and vice versa.

The MPT argues that the risk and return of individual investments should not be viewed alone but should be viewed with their overall impact on the portfolio.

The Core Idea of Modern Portfolio Theory

The central principle of MPT is that the risk and return of an individual investment should not be considered in isolation. Instead, they must be evaluated based on their overall impact on the portfolio. Generally, higher risk brings higher potential reward, but diversification can optimise this balance.

How Does Modern Portfolio Theory Work?

To understand how MPT functions, three key concepts are essential:

Portfolio Return

Portfolio return is the weighted average return of individual investments within a portfolio. This calculation ensures that each asset’s proportionate contribution is factored into overall returns.

Portfolio Risk

Portfolio risk measures the volatility and uncertainty of returns. In MPT, risk is primarily assessed through:

- Alpha and Beta (performance measures)

- Variance and Standard Deviation (spread of returns)

- Value at Risk (VaR)

- R-squared and Downside Risk

MPT considers variance as the main indicator of portfolio risk.

What Is the Modern Portfolio Theory?

TMPT suggests that portfolios with the same risk level can produce different returns. The most efficient portfolio is the one offering the highest return for a specific level of risk.

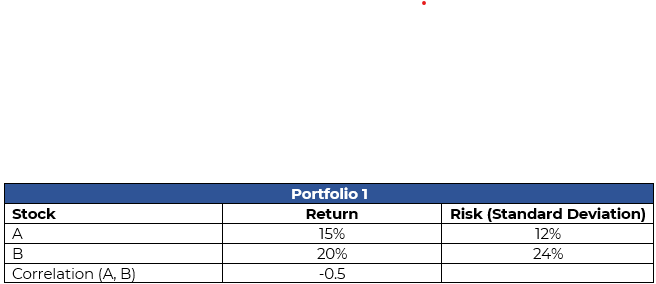

Ex. In a hypothetical universe we have only 2 stocks, Stock A and Stock B. Stock A has historical returns of 15% with standard deviation of 12% and Stock B has historical returns of 20% and standard deviation of 24%. The correlation of Stock A and Stock B is negative 0.5. Now a investor can create different portfolios by combining different weights of these two stocks. Each portfolio will perform based on their weights and will have different risks.

-

Portfolio Return = Weighted Average of Stock A and B

-

Portfolio Risk

(Standard Deviation) =

where σP is the standard deviation of the portfolio. The σa & σb is standard deviation of respective stocks.

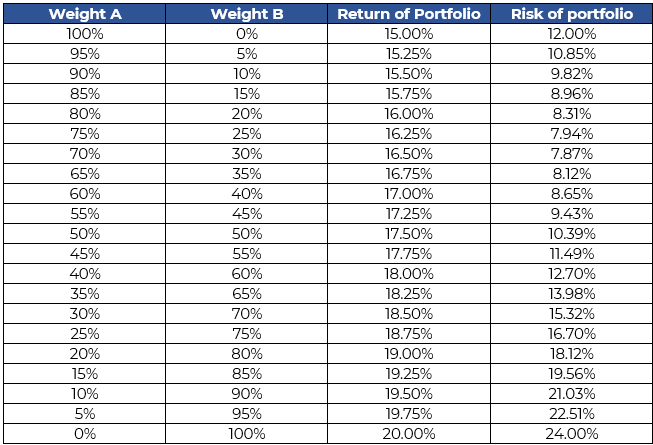

Now the portfolio can be created using stock A and stock B. For this exercise, we have generated a portfolio using different weights of Stock A and Stock B. Similarly, the return and Risk of the portfolio are calculated.

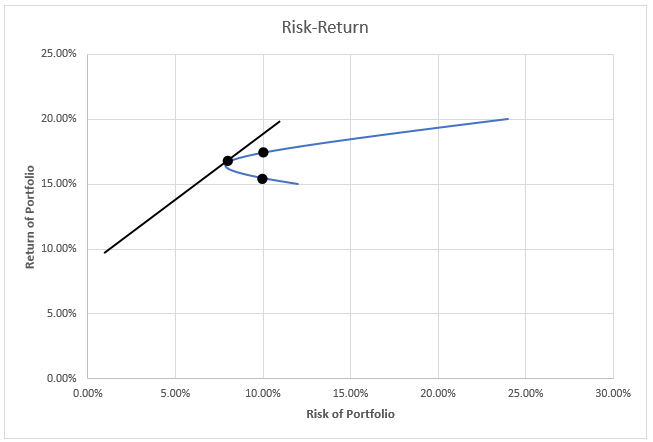

If we plot the graph of the portfolio returns vs portfolio risk. We get –

Here, we can see that at 10% risk 2 different portfolio give 2 different rewards. Thus, Portfolio with higher return is better portfolio.

Efficient Frontier — The portfolios lying on the above curve are efficient portfolios. Further, we can draw line with slope 1, tangent to portfolio to find most efficient portfolio. The point of intersection of the line and curve give us the most efficient portfolio. Beyond this point, marginal increase in risk does not result in proportional increase in return. In simple words, one percent increase in risk leads to less than one percent increase in return.

Drawbacks/Shortcoming of Modern Portfolio Theory –

- MPT relies on historical data, thus it cannot provide guarantee of result in future

- The MPT uses variance as a measure of risk. The theory ignores the downside risk.

Conclusion

The modern portfolio theory is widely accepted in practice. It gives power to individual to diversify the portfolio and generate maximum return for risk potential.